Competitive equilibrium with one-period Arrow securities

1. Competitive equilibrium with one-period Arrow securities¶

1.1. Summary¶

Following descriptions in section 9.3.3 of RMT5 chapter 9, we briefly recall the set up of a competitive equilibrium of a pure exchange economy with complete markets in one-period Arrow securities.

When endowments \(y^i(s)\) are all functions of a common Markov state \(s\), the pricing kernel takes the form \(Q(s'|s)\).

These enable us to provide a recursive formulation of the consumer’s optimization problem.

Consumer \(i\)’s state at time \(t\) is its financial wealth \(a^i_t\) and Markov state \(s_t\).

Let \(v^i(a,s)\) be the optimal value of consumer \(i\)’s problem starting from state \((a, s)\).

\(v^i(a,s)\) is the maximum expected discounted utility that consumer \(i\) with current financial wealth \(a\) can attain in state \(s\).

The value function satisfies the Bellman equation

where maximization is subject to the budget constraint

and also

with the second constraint evidently being a set of state-by-state debt limits.

Note that the value function and decision rule that solve the Bellman equation implicitly depend on the pricing kernel \(Q(\cdot \vert \cdot)\) because it appears in the agent’s budget constraint.

Use the first-order conditions for the problem on the right of the Bellman equation and a Benveniste-Scheinkman formula and rearrange to get

where it is understood that \(c_t^i = c^i(s_t)\) and \(c_{t+1}^i = c^i(s_{t+1})\).

A recursive competitive equilibrium is an initial distribution of wealth \(\vec a_0\), a set of borrowing limits \(\{\bar A^i(s)\}_{i=1}^I\), a pricing kernel \(Q(s' | s)\), sets of value functions \(\{v^i(a,s)\}_{i=1}^I\), and decision rules \(\{c^i(s), a^i(s)\}_{i=1}^I\) such that

The state-by-state borrowing constraints satisfy the recursion

For all \(i\), given \(a^i_0\), \(\bar A^i(s)\), and the pricing kernel, the value functions and decision rules solve the consumer’s problem;

For all realizations of \(\{s_t\}_{t=0}^\infty\), the consumption and asset portfolios \(\{\{c^i_t,\) \(\{\hat a^i_{t+1}(s')\}_{s'}\}_i\}_t\) satisfy \(\sum_i c^i_t = \sum_i y^i(s_t)\) and \(\sum_i \hat a_{t+1}^i(s') = 0\) for all \(t\) and \(s'\).

The initial financial wealth vector \(\vec a_0\) satisfies \(\sum_{i=1}^I a_0^i = 0 \).

The third condition asserts that there are zero net aggregate claims in all Markov states.

The fourth condition asserts that the economy is closed and starts off from a position in which there are zero net claims in the aggregate.

If an allocation and prices in a recursive competitive equilibrium are to be consistent with the equilibrium allocation and price system that prevail in a corresponding complete markets economy with all trades occurring at time \(0\), we must impose that \(a_0^i = 0\) for \(i = 1, \ldots , I\).

That is what assures that at time \(0\) the present value of each agent’s consumption equals the present value of his endowment stream, the single budget constraint in arrangement with all trades occurring at time \(0\).

Starting the system off with \(a_0^i =0 \ \forall i\) has a striking implication that we can call state variable degeneracy.

Thus, although there are two state variables in the value function \(v^i(a,s)\), within a recursive competitive equilibrium starting from \(a_0^i = 0 \ \forall i\) at the starting Markov state \(s_0\), two outcomes prevail:

\(a_0^i = 0 \) for all \(i\) whenever the Markov state \(s_t\) returns to \(s_0\).

Financial wealth \(a\) is an exact function of the Markov state \(s\).

The first finding asserts that each household recurrently visits the zero financial wealth state with which he began life.

The second finding asserts that the exogenous Markov state is all we require to track an individual.

Financial wealth turns out to be redundant.

This outcome depends critically on there being complete markets in Arrow securities.

1.2. Computing and Bellmanizing¶

This notebook is a laboratory for experimenting with instances of a pure exchange economy with

Markov endowments

Complete markets in one period Arrow state-contingent securities

Discounted expected utility preferences of a kind often specified in macro and finance

Common preferences across agents

Common beliefs across agents

A CRRA one-period utility function that implies the existence of a representative consumer whose consumption process can be plugged into a formula for the pricing kernel for one-step Arrow securities and thereby determine equilbrium prices before determing an equilibrium distribution of wealth

Diverse endowments across agents that provide motivations for reallocating goods across time and Markov states

We impose enough restrictions to allow us to Bellmanize competitive equilibrium prices and quantities

We can use Bellman equations to compute

asset prices

continuation wealths

state-by-state natural debt limits

As usual, we start with Python imports

import numpy as np

import matplotlib.pyplot as plt

%matplotlib inline

np.set_printoptions(suppress=True)

1.3. Markov asset prices primer¶

Let’s start with a brief summary of formulas for computing asset prices in a Markov setting.

The setup assumes the following infrastructure

Markov states: \(s \in S = \left[\bar{s}_1, \ldots, \bar{s}_n \right]\) governed by an \(n\)-state Markov chain with transition probability

A collection \(k=1,\ldots, K\) of \(n \times 1\) vectors of \(K\) assets that pay off \(d^k\left(s\right)\) in state \(s\)

An \(n \times n\) matrix pricing kernel \(Q\) for one-period Arrow securities, where \( Q_{ij}\) = price at time \(t\) in state \(s_t = \bar s_i\) of one unit of consumption when \(s_{t+1} = \bar s_j\) at time \(t+1\):

The price of risk-free one-period bond in state \(i\) is \(R_i^{-1} = \sum_{j}Q_{i,j}\)

The gross rate of return on a one-period risk-free bond Markov state \(\bar s_i\) is \(R_i = (\sum_j Q_{i,j})^{-1}\)

At this point, we’ll take the pricing kernel \(Q\) as exogenous, i.e., determined outside the model

Two examples would be

\( Q = \beta P \) where \(\beta \in (0,1) \)

\(Q = S P \) where \(S\) is an \(n \times n\) matrix of stochastic discount factors

We’ll write down implications of Markov asset pricing in a nutshell for two types of assets

the price in Markov state \(s\) at time \(t\) of a cum dividend stock that entitles the owner at the beginning of time \(t\) to the time \(t\) dividend and the option to sell the asset at time \(t+1\). The price evidently satisfies \(p^k(\bar s_i) = d^k(\bar s_i) + \sum_j Q_{ij} p^k(\bar s_j) \) which implies that the vector \(p^k\) satisfies \(p^k = d^k + Q p^k\) which implies the formula

the price in Markov state \(s\) at time \(t\) of an ex dividend stock that entitles the owner at the end of time \(t\) to the time \(t+1\) dividend and the option to sell the stock at time \(t+1\). The price is

Below, we describe an equilibrium model with trading of one-period Arrow securities in which the pricing kernel is endogenous.

In constructing our model, we’ll repeatedly encounter formulas that remind us of our asset pricing formulas.

1.4. Multi-step-forward transition probabilities and pricing kernels¶

The \((i,j)\) component of the \(k\)-step ahead transition probability \(P^k\) is

The \((i,j)\) component of the \(k\)-step ahead pricing kernel \(Q^k\) is

We’ll use these objects to state the following useful facts

1.5. Laws of iterated expectations and values¶

A law of iterated values has a mathematical structure that parallels the law of iterated expectations

We can describe its structure readily in the Markov setting of this lecture

Recall the following recursion satisfied \(j\) step ahead transition probabilites for our finite state Markov chain:

We can use this recursion to verify the law of iterated expectations applied to computing the conditional expectation of a random variable \(d(s_{t+j})\) conditioned on \(s_t\) via the following string of equalities

The pricing kernel for \(j\) step ahead Arrow securities satisfies the recursion

The time \(t\) value in Markov state \(s_t\) of a time \(t+j\) payout \(d(s_{t+j})\) is

The law of iterated values states

We verify it by pursuing the following a string of inequalities that are counterparts to those we used to verify the law of iterated expectations:

1.6. General equilibrium model (pure exchange)¶

1.6.1. Inputs¶

Markov states: \(s \in S = \left[\bar{s}_1, \ldots, \bar{s}_n \right]\) governed by an \(n\)-state Markov chain with transition probability

A collection of \(K \times 1\) vectors of individual \(k\) endowments: \(y^k\left(s\right), k=1,\ldots, K\)

An \(n \times 1\) vector of aggregate endowment: \(y\left(s\right) \equiv \sum_{k=1}^K y^k\left(s\right)\)

A collection of \(K \times 1\) vectors of individual \(k\) consumptions: \(c^k\left(s\right), k=1,\ldots, K\)

A collection of restrictions on feasible consumption allocations for \(s \in S\):

Preferences: a common utility functional across agents \( E_0 \sum_{t=0}^\infty \beta^t u(c^k_t) \) with CRRA one-period utility function \(u\left(c\right)\) and discount factor \(\beta \in (0,1)\)

1.6.2. Outputs¶

An \(n \times n\) matrix pricing kernel \(Q\) for one-period Arrow securities, where \( Q_{ij}\) = price at time \(t\) in state \(s_t \bar s_i\) of one unit of consumption when \(s_{t+1} = \bar s_j\) at time \(t+1\)

pure exchange so that \(c\left(s\right) = y\left(s\right)\)

an \(K \times 1\) vector distribution of wealth vector \(\alpha\), \(\alpha_k \geq 0, \sum_{k=1}^K \alpha_k =1\)

A collection of \(n \times 1\) vectors of individual \(k\) consumptions: \(c^k\left(s\right), k=1,\ldots, K\)

The one-period utility function is

so that

1.6.2.1. Matrix \(Q\) to represent pricing kernel¶

For any agent \(k \in \left[1, \ldots, K\right]\), at the equilibrium allocation, the one-period Arrow securities pricing kernel satisfies

where \(Q\) is an \(n \times n\) matrix

This follows from agent \(k\)’s first-order necessary conditions.

But with the CRRA preferences that we have assumed, individual consumptions vary proportionately with aggregate consumption and therefore with the aggregate endowment.

This is a consequence of our preference specification implying that Engle curves affine in wealth and therefore satisfy conditions for Gorman aggregation

Thus,

for an arbitrary distribution of wealth in the form of an \(K \times 1\) vector \(\alpha\) that satisfies

This means that we can compute the pricing kernel from

Note that \(Q_{ij}\) is independent of vector \(\alpha\).

Thus, we have the

Key finding: We can compute competitive equilibrium prices prior to computing the distribution of wealth.

1.6.3. Values¶

Having computed an equilibrium pricing kernel \(Q\), we can compute several values that are required to pose or represent the solution of an individual household’s optimum problem.

We denote an \(K \times 1\) vector of state-dependent values of agents’ endowments in Markov state \(s\) as

and an \(n \times 1\) vector of continuation endowment values for each individual \(k\) as

\(A^k\) of consumer \(i\) satisfies

where

In a competitive equilibrium with sequential trading of one-period Arrow securities, \(A^k(s)\) serves as a state-by-state vector of debt limits on the quantities of one-period Arrow securities paying off in state \(s\) at time \(t+1\) that individual \(k\) can issue at time \(t\).

These are often called natural debt limits.

Evidently, they equal the maximum amount that it is feasible for individual \(i\) to repay even if he consumes zero goods forevermore.

1.6.4. Continuation wealths¶

Continuation wealths play an important role in Bellmanizing a competitive equilibrium with sequential trading of a complete set of one-period Arrow securities.

We denote an \(K \times 1\) vector of state-dependent continuation wealths in Markov state \(s\) as

and an \(n \times 1\) vector of continuation wealths for each individual \(i\) as

Continuation wealth \(\psi^k\) of consumer \(i\) satisfies

where

Note that \(\sum_{k=1}^K \psi^k = \boldsymbol{0}_{n \times 1}\).

Remark: At the initial state \(s_0 \in \begin{bmatrix} \bar s_1, \ldots, \bar s_n \end{bmatrix}\). the continuation wealth \(\psi^k(s_0) = 0\) for all agents \(k = 1, \ldots, K\). This indicates that the economy begins with all agents being debt-free and financial-asset-free at time \(0\), state \(s_0\).

Remark: Note that all agents’ continuation wealths recurrently return to zero when the Markov state returns to whatever value \(s_0\) it had at time \(0\).

1.6.5. Optimal portfolios¶

A nifty feature of the model is that optimal portfolios for a type \(k\) agent equal the continuation wealths that we have just computed.

Thus, agent \(k\)’s state-by-state purchases of Arrow securities next period depend only on next period’s Markov state and equal

1.6.6. Equilibrium wealth distribution \(\alpha\)¶

With the initial state being a particular state \(s_0 \in \left[\bar{s}_1, \ldots, \bar{s}_n\right]\), we must have

which means the equilibrium distribution of wealth satisfies

where \(V \equiv \left[I - Q\right]^{-1}\) and \(z\) is the row index corresponding to the initial state \(s_0\).

Since \(\sum_{k=1}^K V_z y^k = V_z y\), \(\sum_{k=1}^K \alpha_k = 1\).

In summary, here is the logical flow of an algorithm to compute a competitive equilibrium:

compute \(Q\) from the aggregate allocation and the above formula

compute the distribution of wealth \(\alpha\) from the formula just given

Using \(\alpha\) assign each consumer \(k\) the share \(\alpha_k\) of the aggregate endowment at each state

return to the \(\alpha\)-dependent formula for continuation wealths and compute continuation wealths

equate agent \(k\)’s portfolio to its continuation wealth state by state

Below we solve several fun examples with Python code.

First, we create a Python class to compute the objects that comprise a competitive equilibrium with sequential trading of one-period Arrow securities.

class RecurCompetitive:

"""

A class that represents a recursive competitive economy

with one-period Arrow securities.

"""

def __init__(self,

s, # state vector

P, # transition matrix

ys, # endowments ys = [y1, y2, .., yI]

γ=0.5, # risk aversion

β=0.98): # discount rate

# preference parameters

self.γ = γ

self.β = β

# variables dependent on state

self.s = s

self.P = P

self.ys = ys

self.y = np.sum(ys, 1)

# dimensions

self.n, self.K = ys.shape

# compute pricing kernel

self.Q = self.pricing_kernel()

# compute price of risk-free one-period bond

self.PRF = self.price_risk_free_bond()

# compute risk-free rate

self.R = self.risk_free_rate()

# V = [I - Q]^{-1}

self.V = np.linalg.inv(np.eye(n) - self.Q)

# natural debt limit

self.A = self.V @ ys

def u_prime(self, c):

"The first derivative of CRRA utility"

return c ** (-self.γ)

def pricing_kernel(self):

"Compute the pricing kernel matrix Q"

c = self.y

n = self.n

Q = np.empty((n, n))

for i in range(n):

for j in range(n):

ratio = self.u_prime(c[j]) / self.u_prime(c[i])

Q[i, j] = self.β * ratio * P[i, j]

self.Q = Q

return Q

def wealth_distribution(self, s0_idx):

"Solve for wealth distribution α"

# set initial state

self.s0_idx = s0_idx

# simplify notations

n = self.n

Q = self.Q

y, ys = self.y, self.ys

# row of V corresponding to s0

Vs0 = self.V[s0_idx, :]

α = Vs0 @ self.ys / (Vs0 @ self.y)

self.α = α

return α

def continuation_wealths(self):

"Given α, compute the continuation wealths ψ"

diff = np.empty((n, K))

for k in range(K):

diff[:, k] = self.α[k] * self.y - self.ys[:, k]

ψ = self.V @ diff

self.ψ = ψ

return ψ

def price_risk_free_bond(self):

"Give Q, compute price of one-period risk free bond"

PRF = np.sum(self.Q,0)

self.PRF = PRF

return PRF

def risk_free_rate(self):

"Given Q, compute one-period gross risk-free interest rate R"

R = np.sum(self.Q, 0)

R = np.reciprocal(R)

self.R = R

return R

1.6.7. Example 1¶

Please read the preceding class for default parameter values and the following Python code for the fundamentals of the economy.

Here goes.

# dimensions

K, n = 2, 2

# states

s = np.array([0, 1])

# transition

P = np.array([[.5, .5], [.5, .5]])

# endowments

ys = np.empty((n, K))

ys[:, 0] = 1 - s # y1

ys[:, 1] = s # y2

ex1 = RecurCompetitive(s, P, ys)

# endowments

ex1.ys

array([[1., 0.],

[0., 1.]])

# pricing kernal

ex1.Q

array([[0.49, 0.49],

[0.49, 0.49]])

# Risk free rate R

ex1.R

array([1.02040816, 1.02040816])

# natural debt limit, A = [A1, A2, ..., AI]

ex1.A

array([[25.5, 24.5],

[24.5, 25.5]])

# when the initial state is state 1

print(f'α = {ex1.wealth_distribution(s0_idx=0)}')

print(f'ψ = {ex1.continuation_wealths()}')

α = [0.51 0.49]

ψ = [[ 0. 0.]

[ 1. -1.]]

# when the initial state is state 2

print(f'α = {ex1.wealth_distribution(s0_idx=1)}')

print(f'ψ = {ex1.continuation_wealths()}')

α = [0.49 0.51]

ψ = [[-1. 1.]

[ 0. -0.]]

1.6.8. Example 2¶

# dimensions

K, n = 2, 2

# states

s = np.array([1, 2])

# transition

P = np.array([[.5, .5], [.5, .5]])

# endowments

ys = np.empty((n, K))

ys[:, 0] = 1.5 # y1

ys[:, 1] = s # y2

ex2 = RecurCompetitive(s, P, ys)

# endowments

print("ys = ", ex2.ys)

# pricing kernal

print ("Q = ", ex2.Q)

# Risk free rate R

print("R = ", ex2.R)

ys = [[1.5 1. ]

[1.5 2. ]]

Q = [[0.49 0.41412558]

[0.57977582 0.49 ]]

R = [0.93477529 1.10604104]

# pricing kernal

ex2.Q

array([[0.49 , 0.41412558],

[0.57977582, 0.49 ]])

# Risk free rate R

ex2.R

array([0.93477529, 1.10604104])

# natural debt limit, A = [A1, A2, ..., AI]

ex2.A

array([[69.30941886, 66.91255848],

[81.73318641, 79.98879094]])

# when the initial state is state 1

print(f'α = {ex2.wealth_distribution(s0_idx=0)}')

print(f'ψ = {ex2.continuation_wealths()}')

α = [0.50879763 0.49120237]

ψ = [[-0. -0. ]

[ 0.55057195 -0.55057195]]

# when the initial state is state 1

print(f'α = {ex2.wealth_distribution(s0_idx=1)}')

print(f'ψ = {ex2.continuation_wealths()}')

α = [0.50539319 0.49460681]

ψ = [[-0.46375886 0.46375886]

[ 0. -0. ]]

1.6.9. Example 3¶

# dimensions

K, n = 2, 2

# states

s = np.array([1, 2])

# transition

λ = 0.9

P = np.array([[1-λ, λ], [0, 1]])

# endowments

ys = np.empty((n, K))

ys[:, 0] = [1, 0] # y1

ys[:, 1] = [0, 1] # y2

ex3 = RecurCompetitive(s, P, ys)

# endowments

print("ys = ", ex3.ys)

# pricing kernel

print ("Q = ", ex3.Q)

# Risk free rate R

print("R = ", ex3.R)

ys = [[1. 0.]

[0. 1.]]

Q = [[0.098 0.882]

[0. 0.98 ]]

R = [10.20408163 0.53705693]

# pricing kernel

ex3.Q

array([[0.098, 0.882],

[0. , 0.98 ]])

# natural debt limit, A = [A1, A2, ..., AI]

ex3.A

array([[ 1.10864745, 48.89135255],

[ 0. , 50. ]])

Note that the natural debt limit for agent \(1\) in state \(2\) is \(0\).

# when the initial state is state 1

print(f'α = {ex3.wealth_distribution(s0_idx=0)}')

print(f'ψ = {ex3.continuation_wealths()}')

α = [0.02217295 0.97782705]

ψ = [[ 0. -0. ]

[ 1.10864745 -1.10864745]]

# when the initial state is state 1

print(f'α = {ex3.wealth_distribution(s0_idx=1)}')

print(f'ψ = {ex3.continuation_wealths()}')

α = [0. 1.]

ψ = [[-1.10864745 1.10864745]

[ 0. 0. ]]

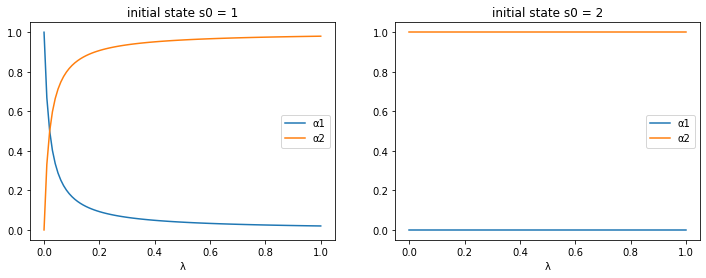

For the specification of the Markov chain in example 3, let’s take a look at how the equilibrium allocation changes as a function of transition probability \(\lambda\).

λ_seq = np.linspace(0, 1, 100)

# prepare containers

αs0_seq = np.empty((len(λ_seq), 2))

αs1_seq = np.empty((len(λ_seq), 2))

for i, λ in enumerate(λ_seq):

P = np.array([[1-λ, λ], [0, 1]])

ex3 = RecurCompetitive(s, P, ys)

# initial state s0 = 1

α = ex3.wealth_distribution(s0_idx=0)

αs0_seq[i, :] = α

# initial state s0 = 2

α = ex3.wealth_distribution(s0_idx=1)

αs1_seq[i, :] = α

<ipython-input-3-1395908c3971>:108: RuntimeWarning: divide by zero encountered in reciprocal

R = np.reciprocal(R)

fig, axs = plt.subplots(1, 2, figsize=(12, 4))

for i, αs_seq in enumerate([αs0_seq, αs1_seq]):

for j in range(2):

axs[i].plot(λ_seq, αs_seq[:, j], label=f'α{j+1}')

axs[i].set_xlabel('λ')

axs[i].set_title(f'initial state s0 = {s[i]}')

axs[i].legend()

plt.show()

1.7. Example 4¶

# dimensions

K, n = 2, 3

# states

s = np.array([1, 2, 3])

# transition

λ = .9

μ = .9

δ = .05

P = np.array([[1-λ, λ, 0], [μ/2, μ, μ/2], [δ/2, δ/2, δ]])

# endowments

ys = np.empty((n, K))

ys[:, 0] = [.25, .75, .2] # y1

ys[:, 1] = [1.25, .25, .2] # y2

ex4 = RecurCompetitive(s, P, ys)

# endowments

print("ys = ", ex4.ys)

# pricing kernal

print ("Q = ", ex4.Q)

# Risk free rate R

print("R = ", ex4.R)

# natural debt limit, A = [A1, A2, ..., AI]

print("A = ", ex4.A)

print('')

for i in range(1, 4):

# when the initial state is state i

print(f"when the initial state is state {i}")

print(f'α = {ex4.wealth_distribution(s0_idx=i-1)}')

print(f'ψ = {ex4.continuation_wealths()}\n')

ys = [[0.25 1.25]

[0.75 0.25]

[0.2 0.2 ]]

Q = [[0.098 1.08022498 0. ]

[0.36007499 0.882 0.69728222]

[0.01265175 0.01549516 0.049 ]]

R = [2.12437476 0.50563271 1.33997564]

A = [[-3.28683339 -1.85525567]

[-2.9759761 -2.70632569]

[ 0.11808895 0.14152768]]

when the initial state is state 1

α = [0.63920196 0.36079804]

ψ = [[-0. 0. ]

[-0.65616233 0.65616233]

[ 0.04785851 -0.04785851]]

when the initial state is state 2

α = [0.52372722 0.47627278]

ψ = [[ 0.5937814 -0.5937814 ]

[ 0. 0. ]

[ 0.01787935 -0.01787935]]

when the initial state is state 3

α = [0.45485896 0.54514104]

ψ = [[ 0.94790813 -0.94790813]

[ 0.39133024 -0.39133024]

[-0. -0. ]]