"""

Inventory management model with state-dependent discounting. The discount

factor takes the form β_t = Z_t, where (Z_t) is a discretization of a

Gaussian AR(1) process

X_t = ρ X_{t-1} + b + ν W_t.

"""

from quantecon import compute_fixed_point

from quantecon.markov import tauchen, MarkovChain

import numpy as np

from time import time

from numba import njit, prange

from collections import namedtuple

# NamedTuple Model

Model = namedtuple("Model", ("K", "c", "κ", "p", "r",

"R", "y_vals", "z_vals", "Q"))

@njit

def ϕ(p, d):

return (1 - p)**d * p

@njit

def f(y, a, d):

return np.maximum(y - d, 0) + a # Inventory update

def create_sdd_inventory_model(

ρ=0.98, ν=0.002, n_z=20, b=0.97, # Z state parameters

K=40, c=0.2, κ=0.8, p=0.6, # firm and demand parameters

d_max=100): # truncation of demand shock

d_vals = np.arange(d_max+1)

ϕ_vals = ϕ(p, d_vals)

y_vals = np.arange(K+1)

n_y = len(y_vals)

mc = tauchen(n_z, ρ, ν)

z_vals, Q = mc.state_values + b, mc.P

ρL = np.max(np.abs(np.linalg.eigvals(z_vals * Q)))

assert ρL < 1, "Error: ρ(L) >= 1." # check r(L) < 1

R = np.zeros((n_y, n_y, n_y))

for i_y, y in enumerate(y_vals):

for i_y_1, y_1 in enumerate(y_vals):

for i_a, a in enumerate(range(K - y + 1)):

hits = [f(y, a, d) == y_1 for d in d_vals]

R[i_y, i_a, i_y_1] = np.dot(hits, ϕ_vals)

r = np.empty((n_y, n_y))

for i_y, y in enumerate(y_vals):

for i_a, a in enumerate(range(K - y + 1)):

cost = c * a + κ * (a > 0)

r[i_y, i_a] = np.dot(np.minimum(y, d_vals), ϕ_vals) - cost

return Model(K=K, c=c, κ=κ, p=p, r=r, R=R,

y_vals=y_vals, z_vals=z_vals, Q=Q)

@njit

def B(i_y, i_z, i_a, v, model):

"""

The function B(x, z, a, v) = r(x, a) + β(z) Σ_x′ v(x′) P(x, a, x′).

"""

K, c, κ, p, r, R, y_vals, z_vals, Q = model

β = z_vals[i_z]

cv = 0.0

for i_z_1 in prange(len(z_vals)):

for i_y_1 in prange(len(y_vals)):

cv += v[i_y_1, i_z_1] * R[i_y, i_a, i_y_1] * Q[i_z, i_z_1]

return r[i_y, i_a] + β * cv

@njit(parallel=True)

def T(v, model):

"""The Bellman operator."""

K, c, κ, p, r, R, y_vals, z_vals, Q = model

new_v = np.empty_like(v)

for i_z in prange(len(z_vals)):

for (i_y, y) in enumerate(y_vals):

Γy = np.arange(K - y + 1)

new_v[i_y, i_z] = np.max(np.array([B(i_y, i_z, i_a, v, model)

for i_a in Γy]))

return new_v

@njit

def T_σ(v, σ, model):

"""The policy operator."""

K, c, κ, p, r, R, y_vals, z_vals, Q = model

new_v = np.empty_like(v)

for (i_z, z) in enumerate(z_vals):

for (i_y, y) in enumerate(y_vals):

new_v[i_y, i_z] = B(i_y, i_z, σ[i_y, i_z], v, model)

return new_v

@njit(parallel=True)

def get_greedy(v, model):

"""Get a v-greedy policy. Returns a zero-based array."""

K, c, κ, p, r, R, y_vals, z_vals, Q = model

n_z = len(z_vals)

σ_star = np.zeros((K+1, n_z), dtype=np.int32)

for (i_z, z) in enumerate(z_vals):

for (i_y, y) in enumerate(y_vals):

Γy = np.arange(K - y + 1)

i_a = np.argmax(np.array([B(i_y, i_z, i_a, v, model)

for i_a in Γy]))

σ_star[i_y, i_z] = Γy[i_a]

return σ_star

@njit

def get_value(v_init, σ, m, model):

"""Approximate lifetime value of policy σ."""

v = v_init

for _ in range(m):

v = T_σ(v, σ, model)

return v

def solve_inventory_model(v_init, model):

"""Use successive_approx to get v_star and then compute greedy."""

v_star = compute_fixed_point(lambda v: T(v, model), v_init,

error_tol=1e-5, max_iter=1000, print_skip=25)

σ_star = get_greedy(v_star, model)

return v_star, σ_star

def optimistic_policy_iteration(v_init,

model,

tolerance=1e-6,

max_iter=1_000,

print_step=10,

m=60):

v = v_init

error = tolerance + 1

k = 1

while (error > tolerance) and (k < max_iter):

last_v = v

σ = get_greedy(v, model)

v = get_value(v, σ, m, model)

error = np.max(np.abs(v - last_v))

if k % print_step == 0:

print(f"Completed iteration {k} with error {error}.")

k += 1

return v, get_greedy(v, model)

# == Plots == #

import matplotlib.pyplot as plt

import matplotlib.pyplot as plt

plt.rcParams.update({"text.usetex": True, "font.size": 14})

# Create an instance of the model and solve it

model = create_sdd_inventory_model()

K, c, κ, p, r, R, y_vals, z_vals, Q = model

n_z = len(z_vals)

v_init = np.zeros((K+1, n_z), dtype=float)

print("Solving model.")

v_star, σ_star = optimistic_policy_iteration(v_init, model)

z_mc = MarkovChain(Q, z_vals)

def sim_inventories(ts_length, X_init=0):

"""Simulate given the optimal policy."""

global p, z_mc

i_z = z_mc.simulate_indices(ts_length, init=1)

X = np.zeros(ts_length, dtype=np.int32)

X[0] = X_init

rand = np.random.default_rng().geometric(p=p, size=ts_length-1) - 1

for t in range(ts_length-1):

X[t+1] = f(X[t], σ_star[X[t], i_z[t]], rand[t])

return X, z_vals[i_z]

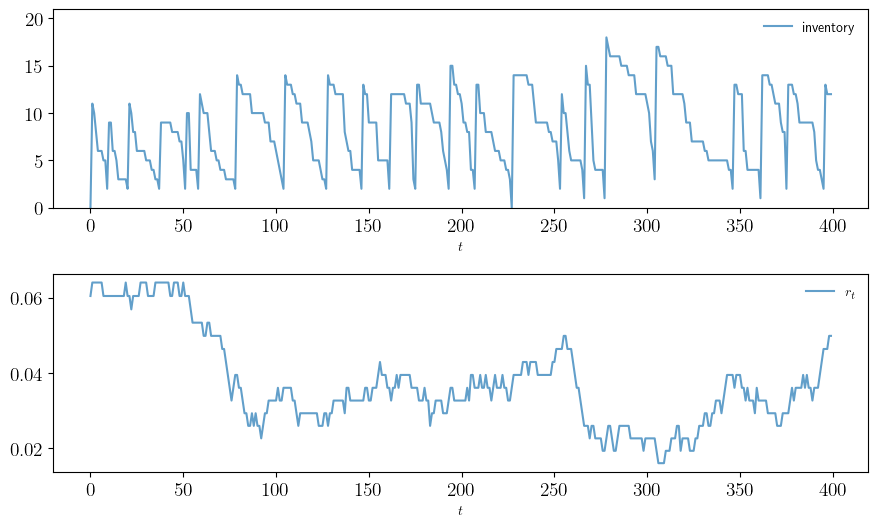

def plot_ts(ts_length=400,

fontsize=10,

figname="./figures/inventory_sdd_ts.pdf",

savefig=False):

X, Z = sim_inventories(ts_length)

fig, axes = plt.subplots(2, 1, figsize=(9, 5.5))

ax = axes[0]

ax.plot(X, label="inventory", alpha=0.7)

ax.set_xlabel(r"$t$", fontsize=fontsize)

ax.legend(fontsize=fontsize, frameon=False)

ax.set_ylim(0, np.max(X)+3)

# calculate interest rate from discount factors

r = (1 / Z) - 1

ax = axes[1]

ax.plot(r, label=r"$r_t$", alpha=0.7)

ax.set_xlabel(r"$t$", fontsize=fontsize)

ax.legend(fontsize=fontsize, frameon=False)

plt.tight_layout()

if savefig:

fig.savefig(figname)

def plot_timing(m_vals=np.arange(1, 400, 10),

fontsize=16,

savefig=False):

print("Running value function iteration.")

t_start = time()

solve_inventory_model(v_init, model)

vfi_time = time() - t_start

print(f"VFI completed in {vfi_time} seconds.")

opi_times = []

for m in m_vals:

print(f"Running optimistic policy iteration with m = {m}.")

t_start = time()

optimistic_policy_iteration(v_init, model, m=m)

opi_time = time() - t_start

print(f"OPI with m = {m} completed in {opi_time} seconds.")

opi_times.append(opi_time)

fig, ax = plt.subplots(figsize=(9, 5.2))

ax.plot(m_vals, np.full(len(m_vals), vfi_time),

lw=2, label="value function iteration")

ax.plot(m_vals, opi_times, lw=2, label="optimistic policy iteration")

ax.legend(fontsize=fontsize, frameon=False)

ax.set_xlabel(r"$m$", fontsize=fontsize)

ax.set_ylabel("time", fontsize=fontsize)

if savefig:

fig.savefig("./figures/inventory_sdd_timing.pdf")

return (opi_time, vfi_time, opi_times)