Exercises¶

Here are some exercises to work through in your own time.

Exercise 4

Using stata fetch the sysauto dataset using

sysuse auto

Part 1:

Use the integrated workflows

to transfer the weight and price variables to python and save the

results in a pd.DataFrame called data.

>>> data

weight price

0 2930 4099

1 3350 4749

2 2640 3799

3 3250 4816

4 4080 7827

.. ... ...

69 2160 7140

70 2040 5397

71 1930 4697

72 1990 6850

73 3170 11995

[74 rows x 2 columns]

Part 2:

Use statsmodels to run a simple OLS regression of weight ~ price

and then run this regression in stata.

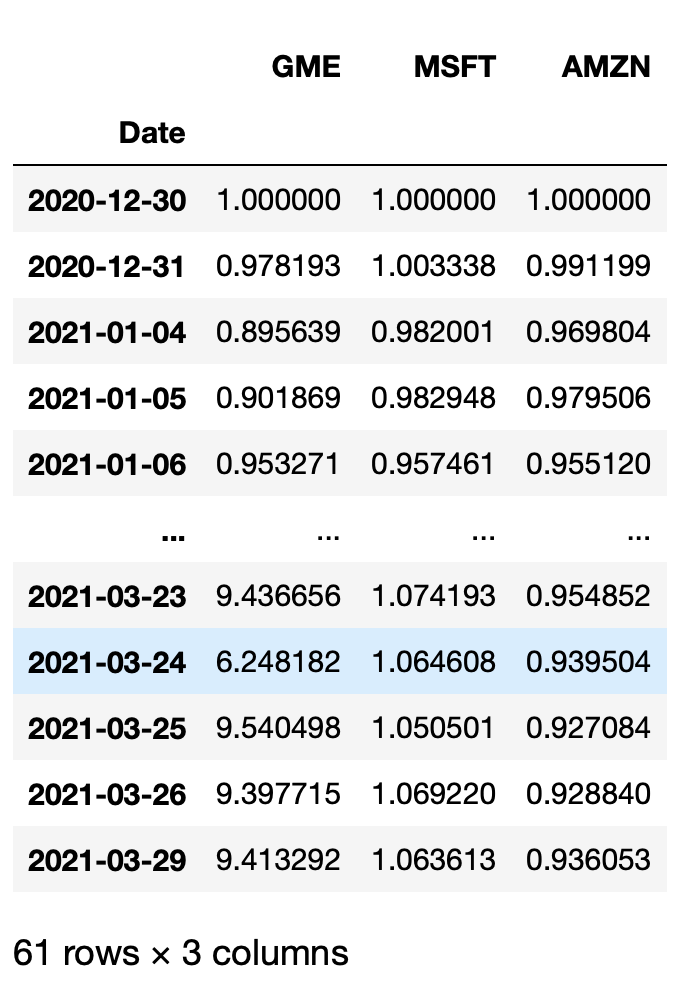

Exercise 5

Use the yfinance package in python to fetch the last 3 months of Close

prince data for:

Amazon (AMZN)

Microsoft (MSFT)

Game Stop (GME)

and construct a dataframe.

Part 1:

Choose to use either the integrated workflows

or file based workflow to transfer the

last three months of stock price data (“closing price”) to stata

Run a simple ols regression:

comparing

AMZNandMSFTstock price historiescomparing

AMZNandGMEstock price histories

Part 2:

Choose either stata or python to normalize each stock price history by

dividing the column by the first price of each stock.

The dataframe should look like

and make a plot comparing the three time series.